Smartphone shipments are shrinking, and the mobile industry faces a new reality. As global demand cools, manufacturers must tackle longer upgrade cycles and macro-economic pressures. Tariff uncertainty—especially in the U.S.—has disrupted supply chains, prompting production shifts to India and Vietnam. Regional trends vary: North America saw early stockpiling, while Europe and Latin America recorded declines of 2–4% .

Meanwhile, China remains flat as domestic brands take over. Amid this slowdown, AI-enabled devices, refurbished phones, and mid-range models offer new growth paths. These evolving currents signal a market pivot—where innovation and adaptability become essential.

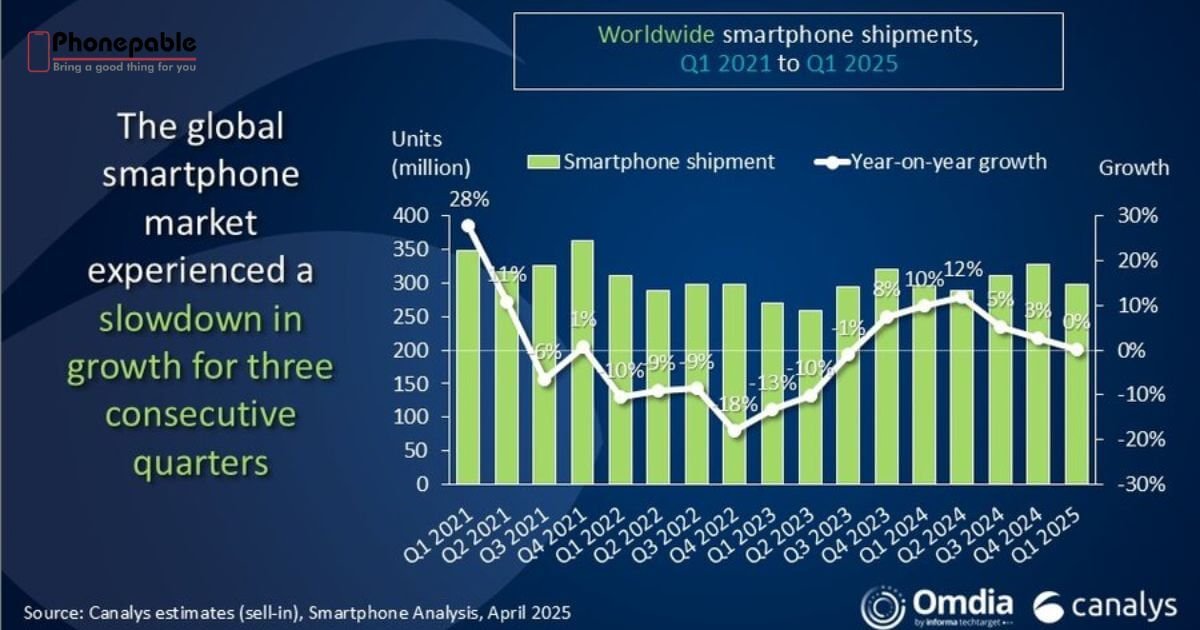

Global Shipment Slowdown: What’s the Big Picture?

Smartphone shipments are cooling after years of rapid growth. According to IDC, growth for 2025 has been slashed to just 0.6%, down from 2.3% earlier forecasts. Counterpoint Research echoes this caution, forecasting only 1.9% growth due to U.S.–China tariff tensions impacting Apple and Samsung. This slowdown reflects longer upgrade cycles, rising device prices, and macroeconomic headwinds that are reshaping demand globally.

Regional Trends: Winners and Losers in Q1 2025

The smartphone market varies sharply by region. In North America, shipments dipped amid price hikes and cautious consumer sentiment. Q1 2025 saw 4% drop in Latin America, hit by inflation and trade disputes. Meanwhile, China eked out slight growth thanks to subsidies, and U.S. Apple shipments rose, fueled by early stockpiling ahead of tariffs . Emerging markets like Africa continue to show resilience, though growth remains uneven.

Brand Battle: Apple, Samsung, and the Chinese Comeback

Apple and Samsung share led shipments but face competitive pressure. IDC noted that in Q4 2024, Apple was down 4.1% while Samsung dropped 2.7%, as Chinese brands like Xiaomi and Oppo surged. Canalys also reported Apple grew 12% in the U.S. in Q1, partly by stockpiling iPhone 16 units. Meanwhile, Huawei gains traction in China, and Xiaomi, Vivo, and Oppo expand aggressively in price-sensitive markets.

Market Saturation & Replacement Cycles: What’s Changing?

Consumers are keeping phones longer, extending replacement cycles. IDC expects a 1.4% CAGR through 2029 due to market saturation and slow refresh rates. Canalys highlights cautious restocking after pandemic-era surges. This entails fewer impulse buys and more strategic purchases of durable, high-quality devices, especially mid-range models that balance performance and price.

Tariff Uncertainty: How Trade Policy Shapes Demand

Tariff threats loom over smartphone pricing. The U.S. considered levying 20–30% tariffs on Chinese imports, prompting temporary pauses . Apple responded by shifting iPhone production to India and Vietnam to avoid higher duties. But uncertainty remains. Analysts warn even rumors of tariffs can stall sales and disrupt consumer confidence, stressing supply chains and pricing models.

Refurbished Market Retreat: Fewer Trade-Ins, Less Supply

Refurbished smartphones are struggling too. In India, organized refurbishers saw a 6% drop in Q1 2025, blamed on fewer trade-ins online, with many devices moving into informal channels. This signals a shrinking secondary market that historically eased strain on younger buyers and reduced e-waste. Ecosystem players may struggle as refurbished supply chains fray.

Future Outlook: Where the Industry Is Heading

Despite setbacks, the industry shows resilience. IDC projects renewed growth post-Q1, helped by new launches and easing inventories . Meanwhile, Counterpoint sees slow-but-steady recovery depending on trade resolution . Key growth drivers: AI-enabled features in phones, expansion in emerging markets, and rising demand for mid-tier devices. Still, higher prices and longer upgrade cycles will temper rapid rebounds.

📊 Table: Q1 2025 Shipment Performance by Region

| Region | Shipment Growth | Key Insight |

| North America | ↑12% (US Apple) | Boosted by early shipments to bypass tariffs |

| China | ~0% | Balanced by subsidies and slower replacement cycles |

| Latin America | −4% | Hit by inflation, Brazil (−7%), Mexico (−12%) |

| Global | +0.4% | Slight annual growth amid soft demand |

Industry Trends to Watch

The smartphone sector is shifting into a maturity phase. Replacement cycles slow, and handset prices rise as tariffs persist. Tier-two brands and refurbished markets face supply issues. Still, AI, 5G upgrades, and mid-range value devices offer tailwinds. How manufacturers adapt pricing, components, and supply chains will determine who thrives.

Frequently Asked Questions (FAQs)

1. Why are smartphone shipments declining?

Rising prices, longer replacement cycles, and macroeconomic pressures are cooling demand.

2. How do tariffs affect shipments?

They raise costs, disrupt supply chains, and force manufacturers to shift production.

3. Which brands are losing market share?

Apple and Samsung face stiff competition from growing Chinese OEMs like Xiaomi and Oppo.

4. Is the refurbished phone market shrinking?

Yes, organized refurbishers saw a 6% shipment decline in Q1 2025 due to fewer trade-ins.

5. Will the smartphone market rebound soon?

Experts see modest growth later in 2025, fueled by new models and easing inventory.